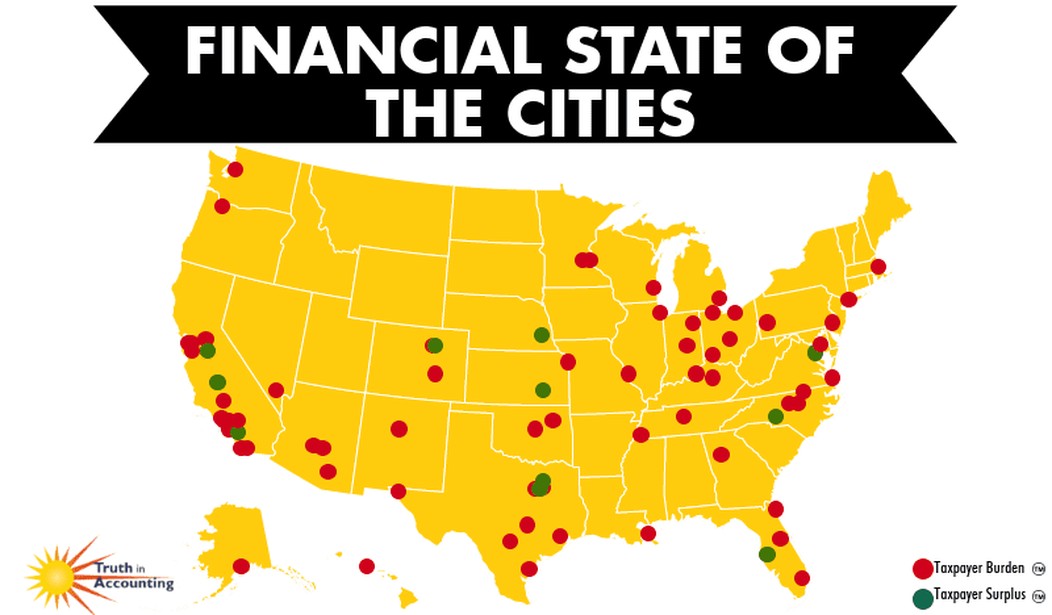

Spoiler alert: almost none of the 75 most populous cities in America have enough money to pay their bills. Overall, those cities have racked up an astounding $335.4 billion in unfunded liabilities. Of that, over $210 billion consists of unfunded pension commitments.

That’s the conclusion reached by Truth in Accounting, a non-partisan think tank that advocates for transparent and honest accounting in public finances. They examined the finances of the top 75 most populous cities in the U.S. and found that 64 of them balanced their budgets only because “elected officials have not included the true costs of the government in their budget calculations and have pushed costs onto future taxpayers.” In addition, one of the top five cities with the best health, Stockton, Calf., garnered an overall grade of B for its fiscal health, but only because they declared Chapter 9 bankruptcy three years before and were able to renegotiate contracts to gain significant debt relief.

This is the second annual Financial State of the Cities report. No city received an A grade this year. Eleven cities earned a B, 23 earned a C, 34 got a D, and 11 got an F.

Notably, two of the largest cities had to be left out of the report. Newark and Jersey City do not issue annual financial statements that follow generally accepted accounting principles (GAAP).

TIA awards letter grades based on the following criteria:

A grade: Taxpayer Surplus greater than $10,000 (0 cities).

B grade: Taxpayer Surplus between $100 and $10,000 (11 cities).

C grade: Taxpayer Burden between $0 and $4,900 (23 cities).

D grade: Taxpayer Burden between $5,000 and $20,000 (34 cities).

F grade: Taxpayer Burden greater than $20,000 (7 cities).

Here’s a handy chart that shows the best and the worst individual debt burdens by city:

Unsurprisingly, Philadelphia, Chicago, and New York City led the way with individual debt burdens over $30,000 per taxpayer. That’s just the municipal burden on individual taxpayers. Those figures don’t include state or federal debt. According to a sidebar on the report, unfunded federal liabilities top out at a staggering $687,000 per person.

It seems like going into debt is all the rage these days.

At least one of the cities in the report that received an F grade, Portland, Oregon, is hitting back. Portland’s debt manager told OregonLive that “the report failed to consider Portland’s unique voter-approved pay-as-you-go tax levy that covers its Portland Fire and Disability Fund. An independent analysis of the levy in June 2016 found that it fully covers future benefits under “a wide range of most likely scenarios.”

He went on to tout the AAA bond rating issued by Moody’s on a variety of bonds issued by the city. Of course, TIA has heard this argument before. The Portland Fire and Disability Fund only funds a portion of the overall pension and benefits burden of the city.

In response to a similar argument made about the State of Delaware, TIA said,

Here are seven ways Truth in Accounting’s (TIA) financial assessments differ from credit ratings:

- Credit ratings are bond-focused.

- State and local government bonds are issued by “sovereigns.”

- Bonds can help kick the can down the road.

- Credit ratings may follow, not lead, real financial deterioration.

- Credit ratings may lag TIA’s Taxpayer Burden.

- Credit rating agencies are paid by governments.

- Credit rating scales themselves may reflect grade inflation / bias. In credit ratings, an “A” is a relatively bad credit. A “BBB” is borderline junk. A “B” is a junk credit. TIA’s grades range from A to F.

You can read the full explanation in detail here.

Truth in Accounting has seen all these tricks before. In fact, that’s why they were founded — to pressure governments to be more transparent and honest in their reporting and accounting. The most common trick they see involves governments shifting some portion of employee compensation off their books. If this were common practice in the private sector, we’d have a lot more Enron situations, and lots more folks would be going to jail.

TIA notes that most city financial reports (again, excluding Newark and Jersey City) were issued about 180 days after year-end. This explains why they are only just now able to offer a report on fiscal year 2016. As they state in the executive summary, most corporations issue their fiscal reports within 45 days of the close of the year. Delays and obfuscations rob taxpaying voters a real opportunity to gauge the performance of elected officials.

So, when you fret about the debt clock that shows us $20+ trillion in debt, don’t forget: that only represents a portion of the burden of each taxpayer.

Here are the 75 cities TIA ranked:

Join the conversation as a VIP Member