eHealthInsurance.com: If you like your plan, you probably won’t be able to keep your plan.

The Obama administration and Health and Human Services Secretary Kathleen Sebelius apparently had no interest in determining the best practices for setting up a health insurance purchasing website before plunging ahead with Obamacare’s.

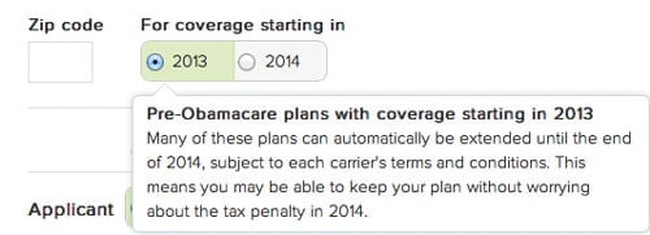

If they did, they might have considered starting at eHealthInsurance.com, which went live in 1998. A quick visit there reminds one of how ridiculously simple all of this currently is — and very soon won’t be, as the screencap at the top of this post illustrates.

Its unstated message is simple: “After 2014, unless Obamacare gets changed, those pre-Obamacare plans will be gone.” Or, more pointedly, “Don’t get too attached to any pre-Obamacare plan you buy, because, contrary to what you were told, you won’t be able to keep it:”

On September 30, the day before HealthCare.gov’s disastrous debut, and after almost four years during which he and his employer danced around and avoided the topic, Calvin Woodward at the Associated Press, aka the Administration’s Press, acknowledged in the sixteenth paragraph of a “fact check” about “slippery claims” that Obama’s “if you like the health care that you have, that you currently have, you can keep it” pledge “was an empty promise, made repeatedly.”

Further, Woodward noted: “Nothing in the health care law guarantees that people can keep the health insurance they already have.”

Translation: “We’ve all known from the start that Obama has been lying to the American people about this, and now that lie has reached the end of its useful life. Too bad, so sad, suckers.”

For a 22-year-old male living in my zip code, answering four questions at eHealthInsurance.com relating to gender, birth date, tobacco use, and student status is all one needs to obtain a list of 70 pre-Obamacare plans offered by five different carriers. Monthly costs range from $40 to $222 per month. Over half are under $100. For a 60 year old, there are also 70 plans and five carriers, with costs ranging from $176 to $913, 50 of which are under $400.

The only credible objection to these arrangements is that those with pre-existing conditions will in most cases be unable to purchase the identified policies. Obama and his administration have tried to scare people about the vast horde of Americans excluded on this basis. But as the Heritage Foundation pointed out earlier this year, the administration’s own attempt to serve affected people until Obamacare officially kicks in “unexpectedly” found far fewer of them, blew through all of its allocated money trying to serve those who did enroll, and had to prematurely shut down new enrollments. (The “party of compassion” strikes again.)

When Obamacare kicks in, there will be no exclusions for pre-existing conditions — and look what will happen to premiums.

The monthly Obamacare price range for the 22 year old is now $142 to $326. The cheapest plan, which by the way comes with a $6,350 deductible, costs more than all but 15 pre-Obamacare policies. About 40 of the 60 pre-Obamacare plans have smaller deductibles than the cheapest Obamacare plan; many are as low as $2,500.

The Kaiser Family Foundation’s Obamacare calculator, which has now been customized to the zip code level since yours truly worked with it in late September, estimates an unsubsidized “Silver Plan” premium of $187 per month ($2,239 per year). The Kaiser model tells us that to get his subsidized premium below the $100 per month mark seen in over half of the non-Obamacare plans, most of which have better coverage, our 22 year old will have to earn $21,300 per year or less, or $10.24 per hour for a full-time worker, assuming no overtime.

How about the 60 year old? Are you sure you want to know?

There are 23 Obamacare plans ranging in cost from $516 to $884. The cheapest Obamacare plan costs more than 56 of the 70 pre-Obamacare plans, and over twice as much as ten of them.

In return for having to pay far more than the private insurance market would charge individuals, the majority of whom, based on the most credible available data, do not have pre-existing conditions, those attempting to enroll in Obamacare, unlike those visiting eHealthInsurance, are being forced to cough up a plethora of personal information before they will receive a quote. One doesn’t have to be paranoid to recognize the fact that the system’s design will enable the government, armed with income-related information, to develop targeted lists of those who have created profiles but haven’t completed their purchase of a legally mandated product.

Unluckily for Team Obama, but perhaps fortunately for what’s left of Americans’ fundamental freedoms, the system’s design probably best explains why its performance has been so abysmal. Generating a quote based on four variables is one thing. Getting one based on dozens of them, accompanied by some attempt at verification — but not too much, based on the administration’s “honor system” posture concerning income-related data for the first go-round — is the $500 million-plus problem.

That’s right. The cost of Obamacare system development thus far, according to Digital Trends, has been over $500 million.

Obamacare has become the Big Dig of systems projects. Subtracting a generous 20% off the top for hardware and other equipment, the cited cost to date means that the government has spent about $400 million on programmers. That’s the equivalent of spending $100 per hour on an army of 1,000 programmers for two full years. What in the world has everyone been doing?

To add insult to injury, the administration outsourced the building of this costly contraption to CGI Group, a Canadian firm. CGI, whose U.S. operations are based in Northern Virginia, “just so happened” to increase the number of H-1B visas it requested from 172 in 2011 to 299 in 2012. It seems more than a little likely that the Obamacare project gave jobs to foreigners while needlessly leaving fully dozens or perhaps even hundreds of qualified citizen IT professionals on the unemployment line.

It gets even worse. CGI was “officially terminated in September 2012 by an Ontario government health agency after the firm missed three years of deadlines and failed to deliver the province’s flagship online medical registry.” Surely someone in the Washington government-media complex knew that CGI had gotten the boot in Ontario. Yet “somehow” this was never news in the U.S. Oh, I forgot. That was less than two months before the presidential election, and there was a blackout on anything not directly involved in trashing Mitt Romney or anyone who might dare support or vote for him.

Obamacare’s enrollment system blowup is all anyone should need to justify delaying the individual mandate for a year to give developers — hopefully news ones — one last chance to get their act together. Or, far better, to give the American people one last chance to elect a Congress and Senate which will do everything it can to end this debacle once and for all.

{kind=link}

Join the conversation as a VIP Member