If the congressional midterms, gubernatorial races, and various state and local electoral contests result in the large-scale repudiation of the left so many are expecting, it will represent only the barest of beginnings towards a genuine long-term national economic recovery.

Only now is it beginning to dawn on many American just how deep our short-term and long-term holes really are. Many others, including politicians who appear to be on their way to key positions after the elections, still don’t seem to get it. This column will focus on the near-term economy — because if we don’t get a handle on a quickly mushrooming mess, and soon, there may not be a long-term.

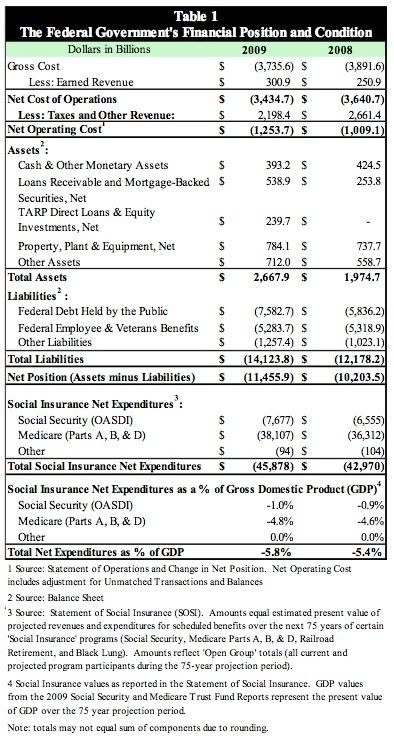

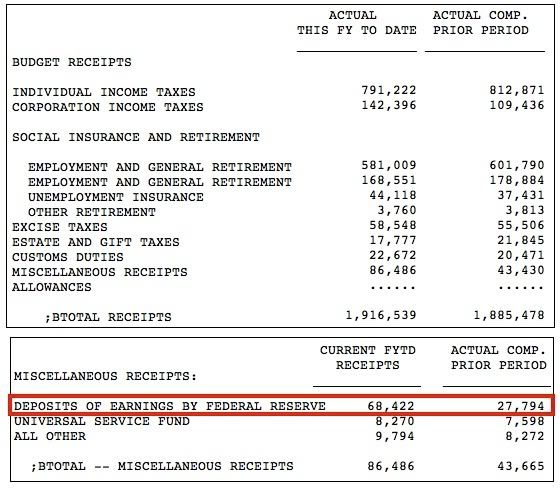

This nation’s government just completed its second fiscal year with deficits of well over a trillion dollars, a number that was unthinkable just two years ago. Despite claims to the contrary, true cash flow from federal government operations during fiscal 2010 was more negative than the previous year. It only looks better because of increased receipts from the Federal Reserve (more on that in a bit) and cleverly manipulated non-cash accounting entries that arbitrarily and artificially reduced this year’s reported outlays. Net tax collections are still about 20% below where they were two years ago, and are only showing bare signs of turning upward.

After separating several stakeholders from billions of dollars to which they were legally entitled during its bankruptcy and creating a new entity with $30 billion of “fluff” known as “Goodwill” on its balance sheet, the government is finding itself saddled with an investment in a giant but shrinking car company which it may be unable to unload, even in part. Uncle Sam is also having a hard time unwinding its “investment” in Citigroup, the bank former Clinton Treasury Secretary Robert Rubin helped bring down, without disrupting the markets.

You’ll have to excuse me for doubting that the Obama administration really wants out of either situation. That’s because they are deliberately diving into the ownership game even further. One example: Almost no one knows that the alleged “small business lending” bill which recently whipped through Congress requires government “capital investment” in participating banks as a precondition for their involvement in the program. Their real objective isn’t small business lending; it’s enlarging the scope of the state’s control.

Speaking of enlargement, has anyone noticed what Ben Bernanke’s Federal Reserve has been up to?

Properly employed, the Fed’s “quantitative easing” (QE) — a euphemism for creating money out of nothing, investing it in government bonds, mortgage-backed securities, and corporate bonds for a while, and then winding those investments down when condition warrant — was supposed to serve as a stabilizing mechanism during the economic recovery. The trouble is that there hasn’t been a meaningful recovery. What little improvement has occurred appears to be stalling out or is at best barely progressing.

This has happened because the administration attempted congenitally ineffective and corrupt “stimulus” programs, enacted a statist health care regime that has left the majority of employer medical plans in a limbo of uncertainty, and has been using the bureaucracy as a weapon against commerce. Beyond that, at any time deemed politically convenient, it has rhetorically bashed and obstructed the productive segments of the private sector, from banking to oil to tourism. An administration and Congress that really cared about inducing a real recovery and reducing the suffering of the nation’s unemployed would at the very least have voted to prevent next year’s scheduled tax increases from taking effect before heading home to defend its electoral turf. Nope.

Ben Bernanke appears to have made the mistake of believing that he was dealing with a rational group of ruling class elites who would change course upon learning that what they had tried didn’t work. He clearly miscalculated.

The administration ignored his July warning before Congress that there was very little the Fed could do to make things better with interest rates already at or near zero. It does not seem to have fazed the remnants of Team Obama that many key economic advisers started jumping ship with what’s left of their reputations rather than become permanently associated with this potential mother of all train wrecks. The two remaining key players, Obama and Treasury Secretary Tim Geithner, seem intent on repeating what hasn’t worked, and won’t work.

Ben Bernanke has been left holding the bag. Rather than allow the markets to collapse, he recently embarked on “QE2,” a second round of easing that will increase the Fed’s investment portfolio.

I fear that Team Obama is starting to like QE, and wouldn’t mind seeing it repeated as many times as necessary until, say, January 19, 2013, or 2017. After all, the larger the Fed’s pool of assets, the greater the income the government collects on its investments. Through August (eleven months of the current fiscal year), Uncle Sam’s receipts from the Fed were up by $41 billion from the same period a year ago. These collections conveniently cover up the fact that five quarters after the alleged recovery began, tax collections from all sources except regular corporations are still down or flat. If QE continues, the administration can go on its merry statist way for two or six more years, while crossing its fingers that good soldier Ben can forestall the inevitable until they leave town. Besides, as Ben’s QE investments expand, the effort begins to look increasingly like a backdoor mechanism for nationalizing the economy. For statists, that’s a feature, not a bug.

QE is in danger of becoming the economy’s crack cocaine. At some point, and it may not be far away, this country’s citizens and the rest of the world — not necessarily in that order — are going to figure out that the habit is unsustainable. The aftermath could get very ugly.

{kind=link}

{kind=link}

{kind=link}

Join the conversation as a VIP Member