Annually for well over a decade, the Social Security system’s trustees have been telling the public in polite words that a) its “trust funds” (old age and disability) represent an accounting fiction, and b) that the time when yearly benefits paid would exceed tax collections is not all that far away.

In a report (large PDF) originating from its Office of Management and Budget (OMB) in 2000, at Page 338, the Clinton White House also acknowledged those verities. Specifically, as the Washington Post’s Charles Krauthammer noted a few weeks ago, OMB analysts wrote:

These balances are available to finance future benefit payments and other trust fund expenditures — but only in a bookkeeping sense. These funds are not set up to be pension funds, like the funds of private pension plans. They do not consist of real economic assets that can be drawn down in the future to fund benefits. Instead, they are claims on the Treasury that, when redeemed, will have to be financed by raising taxes, borrowing from the public, or reducing benefits or other expenditures. The existence of large trust fund balances, therefore, does not, by itself, have any impact on the Government’s ability to pay benefits.

Jacob (“Jack”) Lew was Bill Clinton’s OMB director at the time of that 2000 report. He has held the same job under President Obama since late last year.

For most of the decade which followed, the trustees told us that the Social Security system would begin running cash deficits in the mid- to late-2010s. Then, in the late spring of 2008, along came what I have since been calling the POR (Pelosi-Obama-Reid) economy. The four-quarter recession as normal people define it which Nancy Pelosi, Barack Obama, Harry Reid, and their party caused, followed by the awful policy choices they made once they gained full control over the executive and legislative branches of government, have led to a “recovery” so anemic that, in the words of Mort Zuckerman, the economy “is neither certifiably dead nor robustly alive.”

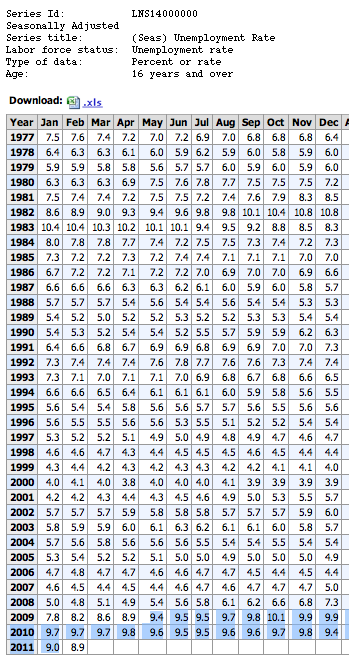

That pathetic “recovery,” accompanied by heavy doses of administration-induced economic uncertainty, has caused unemployment to remain historically high. The 21-month string of seasonally adjusted unemployment rates of 9.0% or higher which finally ended in February is the longest such streak in the 62 years such records have been kept. The government’s Household Survey used to determine the unemployment rate tells us that only 875,000 more Americans were working in February 2011 compared to a year earlier. The Establishment Survey used to report jobs added or lost shows about 1.25 million jobs added; but its figures have been retroactively adjusted downward by hundreds of thousands of jobs in each of the past two years (378,000 in February 2011; 902,000 a year earlier).

The payroll tax receipts on which Social Security depends have plummeted, and remain depressed. Such collections, which amounted to $193.9 billion during the fourth quarter of 2008, came in 6.9% short of that mark at only $180.5 billion in the fourth quarter of 2010, six quarters after the recession ended.

The most recent Social Security Trustees report, issued last year based on the situation at the end of 2009, told us the following:

Social Security expenditures are expected to exceed tax receipts this year for the first time since 1983. … This deficit is expected to shrink substantially for 2011 and to return to small surpluses for years 2012-2014 due to the improving economy.

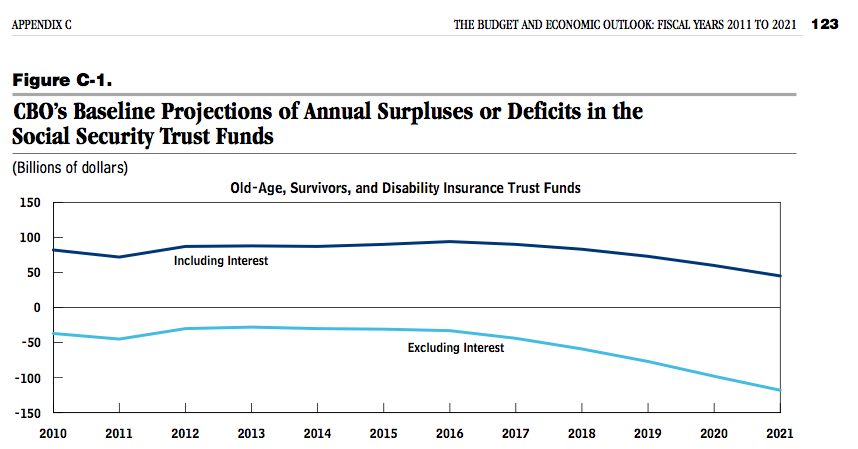

As already seen, the economy in 2010 did not improve in a way that would have helped the Social Security system retain its last shreds of solvency. As a result, the Congressional Budget Office now projects Social Security cash deficits as far as the eye can see, rising from over $40 billion in 2011 to over $100 billion by 2021. Until recently, today’s workers were funding the retirements of today’s retirees. Now generations yet unborn have also been conscripted for that same purpose.

Yet the Obama administration, including the aforementioned, and now about-facing Jack Lew, insists that Social Security must be off-limits in any deficit discussions because, as Lew wrote in response to a USA Today editorial, “Social Security benefits are entirely self-financing.” Suddenly, the “trust fund” which Lew’s 2000 OMB correctly asserted “do(es) not consist of economic assets” is what will in 2011 and beyond enable the system to “have adequate resources to pay full benefits for the next 26 years.”

The 2000 version of Jack Lew was right. Politicians raided Social Security for decades by “borrowing” its surpluses and squandering over $2 trillion. But that wasn’t enough. Except for a brief, primarily Republican-inspired period around the turn of the century, Democratic and Republican administrations have continually added to the nation’s debt load. The Obama administration has taken it to a horrifying new level. By September 2011, it will have rung up over $4 trillion in additional deficits in three fiscal years (it gets responsibility for fiscal 2009 because, as noted earlier, Democrats created the POR economy before that fiscal year began). It has also increased the national debt by roughly $5 trillion.

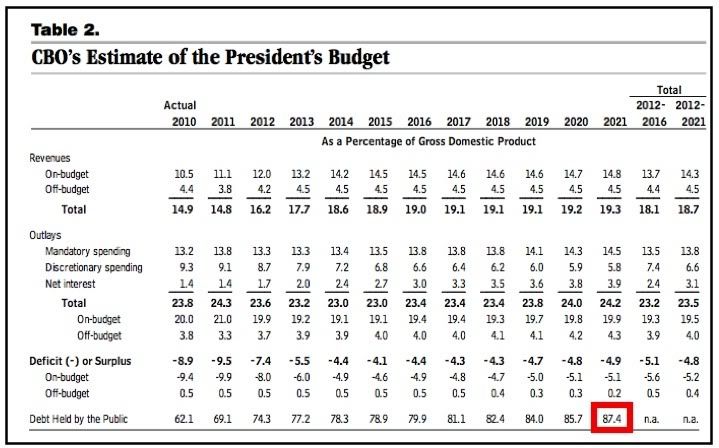

So, if we’re to believe Team Obama, the 2011 version of Jack Lew, and Harry Reid — who doesn’t see a need to deal with Social Security for 20 years — a government whose nonpublic debt is projected to be within a whisker of what many experts believe is the code-red level of 90% of GDP in 10 years is automatically going to be able to continue to fund Social Security’s cash deficits for the next 26 years. Horse manure.

These people know the truth, and they’re deliberately dodging it. They’re cynically hoping to ride a wave of ginned-up opposition to any and all entitlement reform in hopes of getting across the finish line in the 2012 elections. I don’t believe I’ve ever seen a more cynical strategy on a problem so important in my lifetime.

I hope they fail.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Join the conversation as a VIP Member