Last week, the Associated Press’ Jeannine Aversa announced the top ten business stories of 2009, according to an AP survey of newspaper editors.

Not surprisingly, the top story involved the economy. Incredibly, the editors apparently framed it (or maybe the AP framed the survey question for them) as, “Recovery from Great Recession.” Further, Aversa later described the result as “Economy’s Fall — and Rebound.”

This result brings to mind a scene in Breaking Away, a truly underrated movie. In that scene, the story’s lead character Dave (played by Dennis Christopher) begins a brief stint helping out at his father’s (Paul Dooley) used car dealership. It’s brief because when an unhappy buyer returns his vehicle, Dave quickly gives him his money back. Dad’s incredulous response when told is “Refund? REFUND?”

My adverse reaction to Aversa’s description of 2009’s economy is similar to that of Dave’s dad: Rebound? REBOUND?

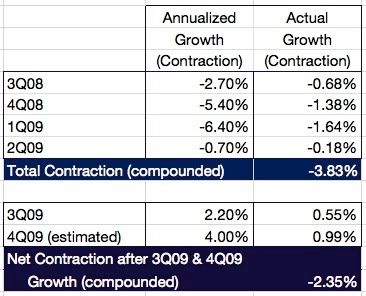

Her assertion is objectively false. You haven’t “rebounded” until you’re back to where you were. Even if economic growth for the fourth quarter comes in at 4% as some predict, the economy won’t even be 40% of the way back from where we were before the recession as normal people define it (“a decline in GDP for two or more consecutive quarters”) began.

More fundamentally, there’s the “little” matter of whether the recession is really over.

As normally defined, the answer of course is simple, which is why we should prefer objective standards for these types of things. The third quarter’s positive annualized growth of 2.2% does indeed mean that the recession ended after four quarters of negative growth that began in July 2008.

But the normal definition is not the one the press has been using. Aversa, AP, and most of the rest of the press have spent the past year telling us that the recession began in December 2007 because the supposedly apolitical academicians at the National Bureau of Economic Research subjectively ignored their own evidence and said so. Now all of a sudden, as seen in this excerpt, Aversa is no longer averse to the normal definition:

After four quarters of decline, the economy returns to growth during the July-to-September period, signaling the end of the deepest and longest recession since the 1930s.

If she were fair, balanced, and consistent, Aversa would be waiting for an NBER determination before concluding that the recession is over. Do you think Jeannine’s shifting definition might have something to do with the fact that it helps Dear Leader?

What’s really offensive about Aversa’s piece is that so many of the other top ten stories reveal how utterly ridiculous her characterization of an economy that is in “rebound” really is.

First, there’s number two, “Auto Industry Collapse.” In November, Chrysler was still collapsing, GM’s year-over-year sales were still declining, and Ford was running just about even. The Japanese trio of Toyota, Honda, and Nissan collectively improved, but total industry sales were flat and not rebounding.

Then there’s number three, “Foreclosures Head Higher.” Aversa herself writes that “by the end of the year, a record 14 percent of homeowners with a mortgage are either behind on their payments or in foreclosure.” That situation is getting worse, not better.

Number five, “Small and Mid-Sized Banks Fail,” is notable because Aversa seems to backtrack on her claim that the recession has ended when she writes that “the banks have been undone by real estate, construction, and industrial loans that soured as the recession has deepened.” Uh, what’s with the present tense?

Aversa also betrays a lack of confidence in number eight, “Federal Aid for Economy,” when she writes that “government stimulus programs spur sales of homes and autos but raise doubts about whether the economic recovery can be lasting if federal aid is withdrawn.” What kind of “rebound” is it if it can’t be sustained without Uncle Sam’s not-unlimited largesse?

I deliberately saved number six, “U.S. Spills Red Ink,” for last. While Aversa dutifully notes the record $1.4 trillion deficit Uncle Sam ran during the past fiscal year, she says it occurred because “financial bailout and war costs soar[ed].” Lord have mercy.

First, as I noted earlier this year, the government began retroactively accounting for the costs of bank, car company, and other bailouts under the Troubled Asset Relief Program (TARP) on a “net present value” basis, thus treating related outlays as “investments” that are not included in current spending. Two non-TARP exceptions to this are Fannie Mae and Freddie Mac, whose bailout costs thus far have exceeded $100 billion. On Christmas Eve, while much of the rest of the nation was engaged in last-minute holiday preparations and enduring airport weather delays, the Obama administration said it would provide the two government wards relief without limits.

Second, “war costs” didn’t “soar.” Total defense spending in fiscal 2009 was only $42 billion higher than it was in fiscal 2008, an increase of just over 7%. Even before determining how much of the increase directly relates to the wars, it accounts for less than 5% of the $962 billion jump in the deficit from the previous year’s $464 billion.

Finally, in addressing the deficit, Aversa missed or ignored an important story the rest of the press neglected, one which deserves its own entry on the list. That story is the catastrophic decline in federal tax and other collections that shows no signs of stopping, let alone “rebounding.”

Tax receipts for calendar 2009 will be about $2.04 trillion. That’s down about $530 billion, or 20%, from calendar 2008 (after adding back that year’s stimulus payments). The steepness of the decline in collections in an economy that contracted less than 4%, and where average employment declined by less than 5%, is proof positive that the “going Galt” phenomenon was very real in 2009.

As long as the administration-fostered atmosphere of uncertainty (yet another missed story) prevails, it will continue.

{kind=link}

Join the conversation as a VIP Member