Many of my conservative friends are spinning their wheels with pea-shooter-gauge measures against China—kicking Chinese companies out of the U.S. stock market, for example. On Dec. 10 the U.S. government canceled an initial public offering for the Chinese AI startup SenseTime, whose facial recognition software may help Chinese authorities identify Uyghurs. Two weeks later SenseTime moved its IPO to Hong Kong; it rose 44% in the first two days of trading. China has a trade surplus, $3.2 trillion in reserves, and a 40% savings rate. It is an exporter, not an importer of capital. American capital markets are a convenience, not a necessity for Chinese companies.

We’ve brought a pea-shooter to a gunfight. There’s a big difference between winning, and making ourselves feel better while we’re losing.

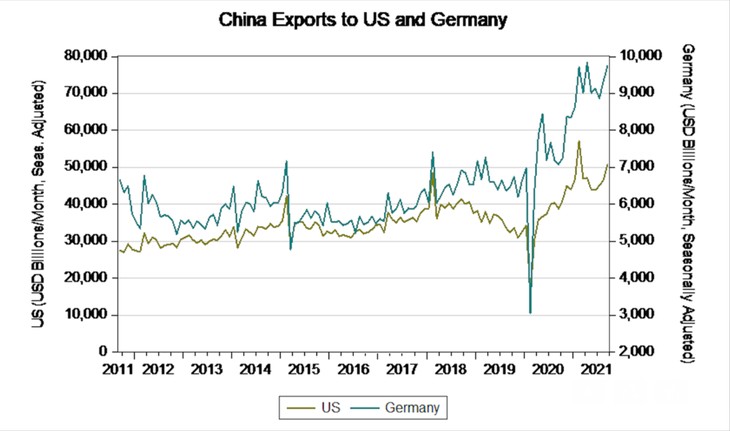

Two charts summarize our position vs. China. The first is Chinese exports to the United States.

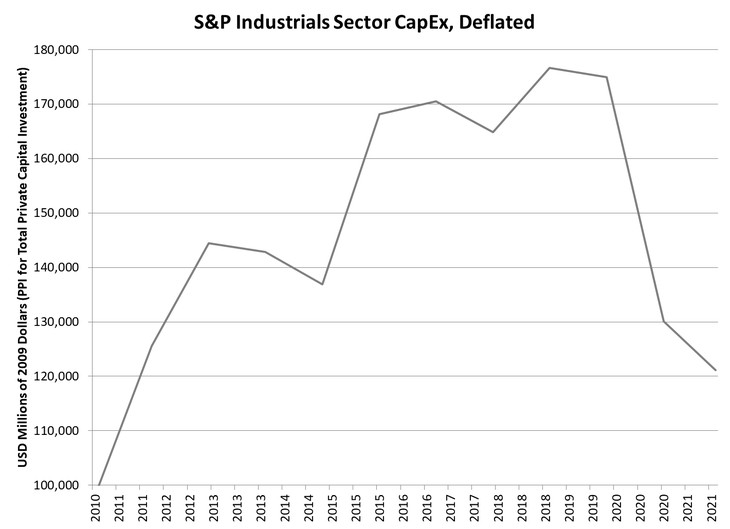

The second is capital spending by U.S. manufacturing companies (the members of the industrials subsector of the S&P 500 stock index), deflated by the Producer Price Index for Private Capital Investment:

Since January 2018 when President Trump imposed tariffs on Chinese imports, our imports from China have risen 30%, to an annual rate of about $600 billion a year—roughly a quarter of the manufactured goods we consume.

During the same period, capital expenditures by U.S. manufacturing companies have fallen from about $170 billion (in 2010 dollars) to $120 billion. That’s total capital spending, including overseas investment, so the actual situation may be slightly better or worse than the aggregate numbers show. Nonetheless, the big picture is dismal.

Complain all you want about China: Its economic power has grown and ours has shrunk. China suppressed the Covid-19 pandemic using Artificial Intelligence analysis of big datasets, along with draconian lockdowns. I broke this story in March 2020. Former Google CEO Eric Schmidt and Harvard’s Graham Allison confirmed my story in August 2020.

Second, China has put vast public resources behind digital infrastructure; it has 70% of the world’s installed 5G broadband capacity and has already automated warehouses and ports.

Either we rebuild American industry and high-tech defense capacity, or we get used to the idea that China will be top dog. We wasted $6 trillion on Forever Wars while China built high-tech weapons including hypersonic missiles (which we can’t get to work yet). Read Graham Allison’s detailed report on the U.S.-China military balance here. Or read a more detailed account in my book, You Will Be Assimilated. If we fight a war near China’s coast now, as Allison documents, we will lose, or go nuclear.

As PJ Media readers know, I supported Donald Trump in both elections and defended him against scurrilous attacks from the Deep State. But his 2018 corporate tax cut was actually Paul Ryan’s tax cut, devised by Big Tech lobbyists. It cut the headline corporate tax rate but withdrew depreciation allowances that encourage capital investment. The next year (2019), U.S. corporations spent more money buying back their own stock than on CapEx. It was great for tech stock prices, not so much for the U.S. economy. Absent investment in U.S. factories, tariffs don’t help. I warned that this would happen in a July 2018 open letter to my friend of many years Larry Kudlow.

I’ve been banging the drum for a high-tech industrial policy now for years, most recently in a monograph for the Claremont Institute’s Center for the American Way of Life. We know how to do it. We’ve done it before. But if we don’t get moving soon, China will be calling the shots, and we’ll only have ourselves to blame.

Join the conversation as a VIP Member