Shortly after Labor Day, as polls continued to sink, the Democratic National Committee (DNC) realized it needed a cash infusion for the upcoming midterm elections. Its chairman, former Virginia Governor Tim Kaine, turned to the Bank of America to secure a $15 million revolving credit line. Then, in the middle of this month, the Democratic Congressional Campaign Committee (DCCC) got another loan from BofA for an additional $17 million.

What was their collateral? It turns out, not much.

The DNC claims their collateral was an intangible piece of property — its donor mailing list. The DCCC only cites unnamed “assets.” Neither party organization possesses real estate even close to cover the $32 million. The DNC’s headquarters is owned by another entity. Even it was put up as collateral, its market value was last estimated at only $13.7 million.

Were the Bank of America deals legitimate, arms-length transactions, or were they cozy sweetheart deals in which nothing was really put up to secure a $32 million loan?

And if it was the latter, could it be considered an illegal campaign contribution from the largest bank holding company in America?

There also is troubling evidence that two days before closing on the loan transaction, the DNC changed its own privacy provisions to allow the selling or sharing of private donor data.

BofA has been a longtime friend of Democrats. In the 2008 election cycle, BofA gave its largest single campaign contribution to then-Senator Barack Obama. According to Bloomberg News, BofA’s new CEO, Brian Moynihan, is considered Obama’s top political ally on Wall Street.

On the eve of the midterm elections, the appearance of preferential loans from cozy Wall Street bankers could play badly with the electorate. What message does a largely unsecured $32 million credit line for the Democratic Party send to thousands of cash-starved small businesses across the nation who can’t secure any credit even with tangible assets?

The findings are part of an exclusive Pajamas Media investigation.

The DNC loan agreement as posted online by the Federal Election Commission (FEC) and signed by former Virginia Governor Tim Kaine (D) on September 16, 2010, says the loan collateral included: “All electronic mail (‘E-mail’) addresses and other contact lists, records and other Information (electronic or otherwise) relating to contributors, supporters and subscribers owned by any of the Borrowers.” The borrowers in this case were the DNC and the DNC Services Corporation.

The loan agreement further stipulates that if the Democrats defaulted, Bank of America would be entitled to “proceeds from any fundraising activity, refunds, reimbursements, or proceeds from the rental or sale of mailing, contact or subscription lists or Information (electronic or otherwise).”

One key to understanding the problems behind the $15 million loan is determining what the donor list is actually worth. The DNC filings with the FEC do not attach any independent appraisal documents or list broker evaluations to establish the list’s fair market value.

Senator John McCain once tried to use his presidential donor list as collateral for a loan. He valued his Republican donor list as worth $3 million. The bank rejected the loan.

Trying to fix a value on an intangible mailing list is very difficult.

“Donor lists do have value, but very fleeting value,” Ken Boehm, chairman of the National Legal and Policy Center, told Pajamas Media. “Lists do deteriorate and $15 million is an awful lot of money. So if the bank ends up with the list because the party is broke, where are they going to get their money?”

A senior executive who is part of a national U.S. bank told Pajamas Media that a data list would be a weak basis for a $15 million loan. He gave his comments on the grounds that he would not be publicly identified. He said he was “somewhat skeptical of a donor list as adequate collateral for a $15 million credit line.”

But if the value is not $15 million, it could be considered a substantial campaign contribution to the Democratic National Committee. And that could be illegal.

“The DNC would have to demonstrate it’s an arms-length, commercially reasonable, properly collateralized loan,” says Cleta Mitchell, a Washington-based attorney with Foley & Lardner LLP and an expert on campaign finance law. She says there needed to be some outside way to assess or appraise the list before the line of credit could be approved. “Otherwise, it’s an illegal contribution from a national bank,” she says.

Hans von Spakovsky, a former commissioner on the Federal Election Commission, agrees. Unless the DNC or BofA conducted an independent appraisal, the loan could be considered an illegal campaign contribution. “The FEC would require an independent appraisal of the fair market value of the list that supports the amount of the loan. Otherwise as a commissioner I would consider this an illegal contribution,” he told Pajamas Media.

In 2005, ATA attorneys for direct mail pioneer Richard Viguerie told the Federal Election Commission that ATA could not get credit using its mailing lists as collateral. Concerning its own client’s many mailing lists, ATA told the FEC that as a standard business practice, “the collateral is the mailing lists. Banks have informed ATA that this is not the type of collateral that banks use to extend credit.”

Without independent documentation, Mitchell told Pajamas Media, “you would never be able to say that their mailing list was worth $15 million. A bank would have to discount the value. So a bank would have to say it was worth at least twice that to get to $15 million.” That, she emphasizes, does require an arms-length appraisal and documentation.

Pajamas Media contacted both the Democratic National Committee and Bank of America for comment and details surrounding the transaction. As of this posting, the DNC has not replied to our inquiries. A communications person from BofA did return our phone call but could not respond to our query. [Update: They did after the piece ran; see addendum below.] She promised she would get someone to respond.

Boehm and Mitchell point out that many campaigns frequently take out short-term, temporary loans as bridge loans until new contributions come in. Most promise to pay it off before the election. The BofA terms are different.

The bank states that the first payment of principal will not be required until February 28, 2011, well after the November elections. Final payment for the debt will not be required until December 2011. What if the party found itself in deep debt after losing one or both houses of Congress?

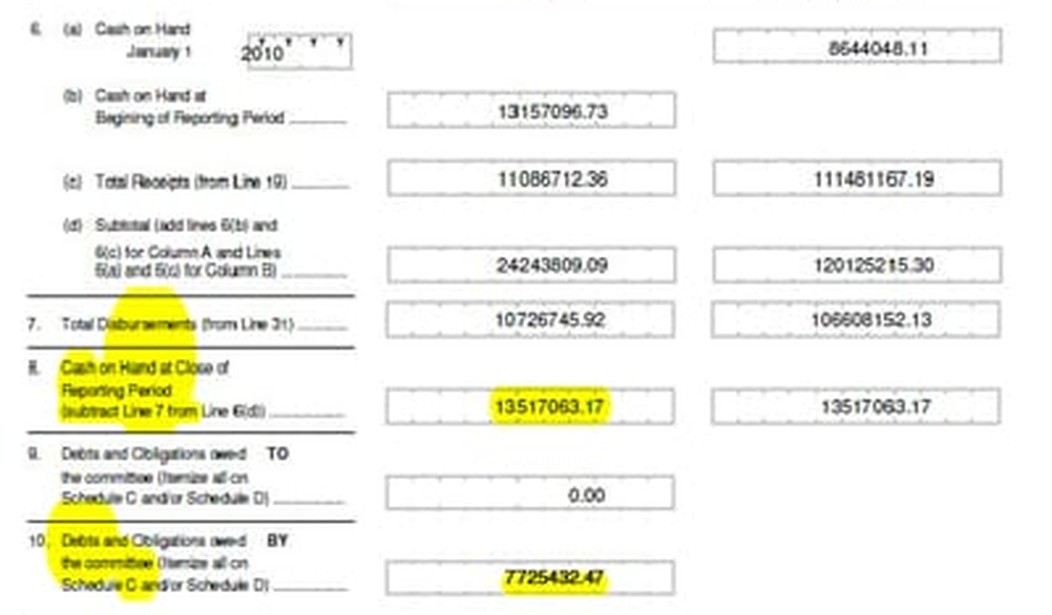

As of October 13, the DNC reported $13.5 million of cash on hand with debts of $7.7 million. Their total worth was $5.8 million with three more weeks of campaigning ahead. (The Democratic Congressional Campaign Committee took out an additional $17 million credit line on October 21.)

There is also the issue of whether on the eve of the loan, the Democrats altered their own privacy policy about sharing private donor data. On September 14, two days before executing the loan, the DNC changed its privacy policy web page. The site initially states that their privacy policy is not to share private data: “It is our policy not to share the personal information we collect from you.”

However, the site adds in its last line that indeed it might share private information if it is the result of an “asset sale or in any other situation where personal information may be disclosed or transferred as one of the assets of the DNC.”

Is it simply a coincidence that the last item of this section acknowledges the DNC might share private information as a result of an asset sale to a third party? Or was it added to accommodate the new collateralized loan?

Other Democratic Party web sites strictly forbid the sharing of their mailing lists unless authorized by the individual. For example, one local Democratic website directly state to its supporters: “We will not give, sell or rent your email address to any other organization unless you specifically authorize us.”

The Democrats’ long-time sweetheart relationship with the banking world and with the Bank of America in particular creates the appearance of an insider deal.

BofA was very generous to Barack Obama when he ran for President. Campaign finance records show that in the 2008 election cycle, Senator Barack Obama was the top recipient of Bank of America campaign donations, reaping $421,000.

BofA’s new CEO, who took over from embattled Kenneth Lewis, is considered one of the Obama administration’s top Wall Street allies on a whole host of issues, from the creation of a consumer regulatory agency to the defense of the administration’s home mortgage fiascoes.

Here’s what Bloomberg News reported about the Moynihan-White House axis last May when he was the number two at BofA:

“He has been willing to speak out bravely in his industry on the need for reform measures,” says Valerie Jarrett, Obama’s liaison to corporate America who has met with Moynihan at the White House several times. “And he has been willing to come to Washington and roll up his sleeves and work on the issue.”

The history between BofA and Democrats goes back years. One highly publicized political scandal linked the bank and Democrats to the subprime mortgage giant Countrywide Financial, which BofA acquired more than two years ago. Countrywide CEO Angelo Mozilo gave preferential below market mortgages to leading Democrats like Connecticut Senator Chris Dodd, the chairman of the Senate Banking Committee. After the disclosure of the mortgage favors, both Dodd and Senator Kent Conrad (D-SD) decided not to run for re-election.

Dodd and other Washington Democrats belonged to a group of VIP loan recipients known in company documents and emails as “FOAs” — Friends of Angelo, a reference to Angelo Mozilo.

“This (type of loan) isn’t something that’s generally offered to the general public, but it looks like it is something of a sweetheart deal,” observes Boehm about the new BofA credit line to the DNC. “Usually when you see this it is banks with a relationship with candidates and we see that all over the place. We saw that with Countrywide,” he told Pajamas Media.

Allowing third parties access to donor mailing lists as part of financial transactions can be tricky business. For years Democratic activists hounded Republican Sen. John Ashcroft about the third party use of his mailing list. The Federal Election Commission fined his campaign $37,000.

The issue may not play well with voters either. Getting an easy line of credit may not sit well with cash-starved small businesses that have sought loans during the bad economy — even when they tried to collateralize it with real, not abstract assets.

The question is, will the DNC come clean and open their books on the transaction?

Update: Jefferson George, a Bank of America spokesman, responds:

First, the answer to the question raised in the headline – “Did the DNC Get an Illegal Campaign Loan from Bank of America?” – is no. We follow all Federal Election Commission guidelines in our financial transactions with political parties and apply the same underwriting standards to these organizations as we do to any other institutional borrower. We also work closely with outside campaign finance legal experts to structure and document these transactions. These agreements are required to be arms-length transactions, and we are very careful with how we underwrite these loans.

As I mentioned, we have always had relationships with committees that represent political parties on both sides of the aisle. Our banking relationship with the Democratic Party dates back more than 30 years, well before the current administration. We also have provided loans for Republican candidates and committees. For instance, we provided financing for Mitt Romney’s 2008 presidential campaign.

Regarding the loans to the DNC and DCCC, due to client confidentiality obligations, we can’t discuss specific loans publicly beyond what is disclosed by the FEC, and we would refer you to those individual organizations. We can say, however, that collateral for these types of loans may include many things, and donor lists usually are insignificant compared such security measures as blanket liens against all assets, including accounts receivable. This also assumes a client doesn’t have adequate cash flow from the collection of contributions. Other factors in considering a loan include a client’s history with repaying loans on time or ahead of schedule.

Update (5:10 PM PDT): More from Jefferson:

Thanks for this. Saw the updated story. One clarification, and it was my error: We didn’t provide financing for Romney. Rather, we had — and have — a banking relationship, handling deposits and providing other cash management services. And that relationship is still active.

Update (8:00 PM PDT): Richard Pollack adds:

The nub of the story is that Bank of America refuses to confirm that an independent appraisal was done for the issuance of two huge loans to the Democrats totaling $32 million. While the bank might wish to invoke confidentiality, in the post-partisan era promised by President Obama, transparency around this particular loan is vital. This is especially true if there are allegations of violations of law.

The scope of the BofA small business loan to the Democrats is breathtaking. According to CNN/Money, in 2009, the bank issued 308 loans to small businesses totaling $17.6 million and in 2010 it issued 185 loans totaling $22.8 million. So the size of the Democrats’ two loans dwarfs all loans to small businesses in each calendar year. I wonder how credit-starved small business owners would feel about these Democrat loans tonight.

In that CNN/Money article, Mr. George was interviewed, saying, “Among those seeking loans, the creditworthiness of many businesses has changed. Cash flow — the most important factor — often is down. The value of collateral, such as real estate or equipment, has decreased.”

Mr. George had it right. Collateral is everything. The public has a right to know what is the collateral behind the $32 million in loans. Otherwise, it can be regarded as a gift, and patently illegal under federal campaign finance laws.

(Update: 7:54 AM PDT, 10/28): More from Jefferson:

Your last update at 8:00 pm ET is incorrect. The numbers you cite from the CNN/Money story are for SBA loans. That was clearly stated in the story, and SBA lending is a very small percentage of Bank of America’s total lending to small businesses. In 2009, Bank of America loaned $16.5 billion to small businesses. Through the third quarter of 2010, Bank of America loaned $13.9 billion to small businesses.

Beyond direct lending, Bank of America works with Community Development Financial Institutions (CDFIs) to provide financing and technical assistance to businesses that don’t qualify for traditional financing. As the leading financial institution supporting CDFIs, the bank provides $1 billion of capital – including more than $200 million to CDFIs that finance small businesses in lower-income communities. Bank of America also recently launched a grant program for CDFIs and other nonprofit lenders, aimed at unlocking $100 million in low-cost, long-term capital for small and rural businesses. To date, the bank has awarded grants that allowed CDFIs to access nearly $27.5 million in lending capital.

In addition, Bank of America has made a commitment to increase spending with small, medium-sized and diverse businesses. The bank’s pledge to purchase $10 billion in products and services from those suppliers over the next five years will provide much-needed income for those businesses. Finally, Bank of America recently announced it will hire more than 1,000 Small Business Bankers by early 2012. Based in communities across the U.S., these bankers will consult with small business owners, spend time at their offices and assess their companies’ deposit, credit and cash management needs.

(Update:7:56 AM PDT, 10/28): Richard Pollock responds:

Thank you for your additional comments on behalf of Bank of America. We will post them in full.

As for the substance of your comments:

Actually, I understated the case in your favor by citing the CNN/Money figures. These loans are not to your smallest business customers, which are really hurting in the credit crunch. It’s your biggest SBA (7) loan portfolio, which is the government backed loan program for small businesses through the Small Business Administration.

Your $32 million dwarfs those loans, many of which have been in trouble because of deterioration in collateralized assets. Your former CEO, Ken Lewis, has admitted this repeatedly. That’s why more conservative rules need to be applied in this economic downturn, not more relaxed standards. The Democratic National Committee and the DCCC will continue. No doubt. But its indebtedness after its most expensive and probably losing mid-term election cycle may put it in a precarious state until the presidential campaign. If may twist on an old financial cautionary warning: past performance is not a guarantee of future results. In 2010, the DNC and the DCCC may face substantial indebtedness and will have to repay the loan through 2012 as well as re-build their donor base.

I strongly recommend that your urge your clients, the DNC and DCCC, to be transparent and back up the collateral for their $32 million lines of credit. Failure to do so will only give the public the impression that there was a sweetheart deal here, and perhaps even the appearance of unlawful activity as well.

irst, the answer to the question raised in the headline – “Did the DNC Get an Illegal Campaign Loan from Bank of America?” – is no. We follow all Federal Election Commission guidelines in our financial transactions with political parties and apply the same underwriting standards to these organizations as we do to any other institutional borrower. We also work closely with outside campaign finance legal experts to structure and document these transactions. These agreements are required to be arms-length transactions, and we are very careful with how we underwrite these loans.

As I mentioned, we have always had relationships with committees that represent political parties on both sides of the aisle. Our banking relationship with the Democratic Party dates back more than 30 years, well before the current administration. We also have provided loans for Republican candidates and committees. For instance, we provided financing for Mitt Romney’s 2008 presidential campaign.

Regarding the loans to the DNC and DCCC, due to client confidentiality obligations, we can’t discuss specific loans publicly beyond what is disclosed by the FEC, and we would refer you to those individual organizations. We can say, however, that collateral for these types of loans may include many things, and donor lists usually are insignificant compared such security measures as blanket liens against all assets, including accounts receivable. This also assumes a client doesn’t have adequate cash flow from the collection of contributions. Other factors in considering a loan include a client’s history with repaying loans on time or ahead of schedule.

Join the conversation as a VIP Member